When analyzing stocks or assets in general, you have two main options: technical analysis or fundamental analysis. In simple terms, technical analysis is analyzing the price chart without knowing much about the company itself. Fundamental analysis is the complete opposite. You actually do not have to look at the price chart but analyze everything around the company itself. With fundamental analysis, you try to come up with your own “fair” value of the stock by analyzing related economic, financial, and other qualitative and quantitative factors. This includes studying a company’s financial statements, understanding its earnings, expenses, assets, and liabilities, and comparing it with its competitors and the overall market.

In short, fundamental analysis should help the investor to make a rational investment decision.

In this article, we will try to give the most important information on fundamental analysis in a condensed way, accompanied by a variety of examples and quotes from famous investors:

- Key Concepts of Fundamental Analysis

- Qualitative Analysis

- Quantitative Analysis

- Valuation Methods

- Risks Involved in Fundamental Analysis

- Conclusion

Key Concepts of Fundamental Analysis

Intrinsic Value

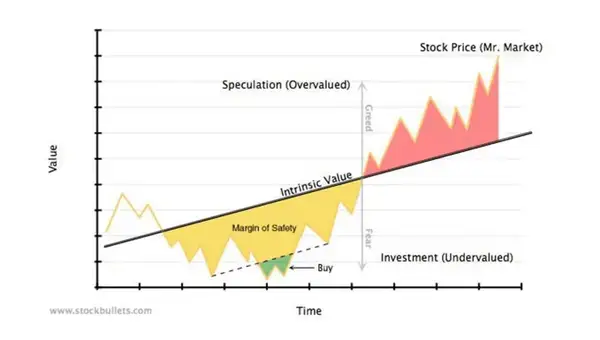

This is one of our favourite charts, as it clearly shows what intrinsic value is. A picture says more than a thousand words, right?

The intrinsic value of a stock is sort of the “real” value of a stock, which is not based on its current market sentiment price but rather on its fundamentals like earnings, dividends, and growth rate.

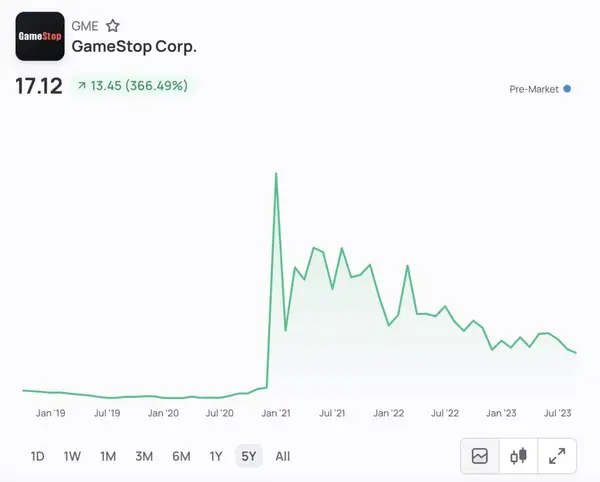

Think about it this way. Sometimes the stock market has an emotional reaction to any short-term news that clickbait media throws at us. However, that actually does not change the underlying “intrinsic value” of the stock. GameStop skyrocketed from around $2 per share to $80 per share in a couple of days and then fell to $25 a month later. Did the company grow their operations so quickly these days that the share price got so high? The obvious answer is “No”. Did the business make much less money in the month after the share price fell from $80 to $25? No. Probably, the fundamentals in this period did not change at all. The price swings are just games of the stock market and investor sentiment. In the long run, the intrinsic value of the stock seems to be somewhere in the middle.

Hence, our goal with fundamental analysis is to find the intrinsic value of the stock and invest accordingly. With this concept, you do not care about short-term price swings, as your analysis shows that the stock will revert to a certain “intrinsic value” price in the long run.

“I’m not emotional about investments. Investing is something where you have to be purely rational and not let emotion affect your decision making – just the facts.”

Bill Ackman

Value vs. Growth Investing

Now that we understand the crucial concept of intrinsic value, we will branch out and seek different variations of fundamental analysis: value vs. growth.

Value Investors want to find companies that they think are undervalued, so stocks that sell less than their intrinsic value. Growth investors, on the other hand, search for companies that exhibit signs of above-average growth.

A metric both investors might use is the Price-to-Earnings ratio (P/E). A high P/E ratio can mean that a stock's price is high relative to earnings and possibly overvalued. A low P/E ratio might indicate that the current stock price is low relative to earnings.

The value investor is seeking stocks with a low P/E ratio and would not go for a stock that has a high P/E ratio. The growth investor would probably still buy the stock, even if the current P/E ratio might seem high.

To characterize the two types even better, we would like to give you an idea of what companies a value investor vs. a growth investor might be buying.

- A value investor might look for an established manufacturing company that is temporarily facing some kind of issues. For such a company, the short-term stock price is probably below the intrinsic long-term value. If the value investor believes that the issues will be resolved, he is firm that the stock price will converge back to the intrinsic value price over the long run.

- A growth investor, however, would instead pick a tech startup with a groundbreaking new product and rapidly increasing revenues or network effects.

A big difference between value and growth investing can often be seen in a metric called the P/E ratio. A high P/E ratio or Price to Earnings ratio might indicate that a stock's price is high relative to earnings and possibly overvalued. In general, a value investor would rather stay away from companies with high P/E ratios, but a growth investor might still make the investment.

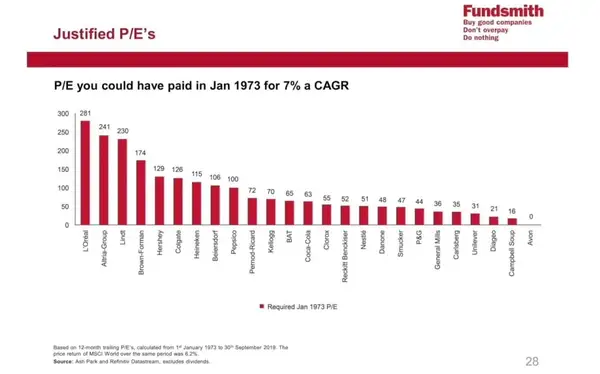

Throughout history, there have been several companies that actually had really high P/E ratios, but still turned out to be great investments bringing in over 7% Compound Annual Growth Rates.

“Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much difference than a 6% return—even if you originally bought it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive-looking price, you’ll end up with a fine result.”

Charlie Munger

Charlie Munger

Margin of Safety

Finally, before we get into how to use fundamental analysis exactly, we want to touch briefly upon the so-called “Margin of Safety”. Seth Klarman, a famous investor, actually wrote a whole book about that concept, and the main idea is to buy with a bit of extra cushion. The extra cushion around the price is important to account for unknowns and biases. Fundamental analysis helps us to generate an intrinsic price. However, it is not a precise value. The intrinsic price is our personal approximation and is, thus, unfortunately, prone to our biases. Knowing that we might not have all the answers and can sometimes be overconfident is really important. If we ignore this, it could lead to trouble. By staying humble but confident and being careful with our hopes and plans, we work our way through the uncertainties of investing. Hence, you should always keep in mind the safety net that the Margin of Safety provides us.

With this general knowledge of fundamental analysis, we are now ready to go into further detail. Within fundamental analysis, besides the value and growth distinction, you have multiple angles on how to approach your analysis. In fact, there is no limit to the degree of detail your analysis could go into. However, when doing your analysis, it is convenient to put your information in quantitative and qualitative groups.

Qualitative Analysis

Qualitative factors explore various aspects such as the kind of business, the company's standing in the industry, its location, how it operates, management quality, and the future prospects for the company, the industry, and the business overall. Typically, company reports don’t address these questions. To find answers, you have to turn to diverse information sources, which can vary widely in reliability and often include a substantial amount of subjective opinions.

Company Management

How would you characterize good management? This is an extremely difficult task and cannot be properly quantified. There are many stories where star CEOs were actually frauds, like in the case of Theranos, Wirecard or FTX. Also, great CEOs were often discredited, like Steve Jobs, who was even fired from Apple at some point, or Elon Musk, whose company was often the most shorted company in the world. Everyone has their own ways of accessing good management. However, a good point to start is always to see their past record.

By analyzing documents and statements made by the CEO, you might get insights into their honesty, reliability, and whether they fulfil their promises regarding the company’s condition and future prospects. However, it might be smart to go even further, and even watch interviews and press conferences to better know the CEO.

Think about CEO research like Grand Admiral Thrawn, a great but fictional tactician from Star Wars, thinks about his enemies: “Thrawn’s strongest belief was that one must know their enemy in order to achieve victory in war. As such, he spent much of his time studying and understanding the art, philosophy, and culture of his opponents.”

Another thing to consider is perhaps real experience; is the CEO a real expert or just an operator. What were his achievements in the past – did he found or inherit? Will he be able to steer the company in the right direction if a crisis comes?

“When an heir inherits an institution, it's like inheriting a factory. During normal times it continues to run…but something important has been silently lost — the founder's ability to invent the institution from scratch or reinvent it in a crisis.”

Business Model

Now, onto the business model, the company's heart, which ties every part of the business together. If you ask what distinguishes a good business model from an average one, we cannot give you a clear answer. Sometimes, it might be the distribution, and sometimes it might be a great product, but in general, there is always some sort of “unfair advantage” that a company has that allows it to be superior.

Let us give you some examples. There are great medical companies out there with potentially cheap and life-saving medicine. However, other big pharma companies block their way to market with different regulations. Even though the big pharma companies do not have superior products, they have an unfair business model advantage. Another example would be companies like Apple or Coca-Cola. Both of these companies have an unfair business model advantage against other companies in their industry due to their strong brand. Thus, they are able to charge higher prices, and people will still buy the product.

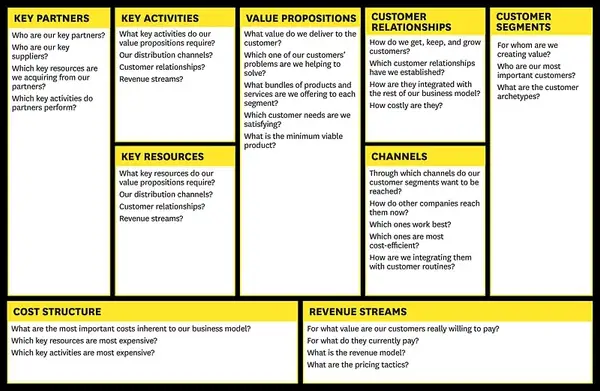

There are different types of analysis you can use for business models. Generally, Michael Porter is one of the Gurus in this field, and his frameworks, like the 5 Forces, are used to this day.

We like a more modern approach with new models developed by a company called Strategyzer. They took the original research of Porter and gave it a modern spin to analyze business models holistically. Perhaps it is not necessarily a better way to think about business models, but an easy and differentiated approach.

There are multiple other frameworks and tools to analyze business models, such as:

- SWOT Analysis

- PESTLE Analysis

- BCG Matrix

- Value Proposition Canvas

- Business Model Canvas

- Environment Map

- Portfolio Map

Another valuable method for investors is the Scuttlebutt technique, proposed by Phil Fisher. This method encourages a journalistic approach to investing, involving further research beyond official sources. It involves examining a cross-section of opinions from various stakeholders related to a company to construct a well-rounded picture of its strengths and weaknesses.

Go ahead and try to analyze the business from various perspectives, but remember to look for that one distinguishing characteristic between mediocre and great businesses: the unfair advantage.

Quantitative Analysis

Quantitative analysis includes all the helpful details about the company’s finances, such as income and balance sheet, along with extra information about things like how much is being produced, the prices of units, costs, capacity, and any orders that haven’t been filled yet. These details can be grouped into four categories:

- Capitalization: This is about how the company is funded, including both debt (like loans) and equity (like stocks).

- Earnings and Dividends: This section talks about the company's profits (earnings) and the portion of those profits given back to stockholders (dividends).

- Assets and Liabilities: Here, you'll find information on the company's assets (what it owns) and liabilities (what it owes).

- Operating Statistics: This category includes various data about the company’s day-to-day operations, like production levels and order status.

These categories help organize the information to make it easier to understand the company’s financial situation and performance. But where should we start, and how can we get these things?

Don’t panic; luckily, there are rules in place that these big companies have to publish their numbers so everyone can check them. The company’s financial documents are usually available in the investor relations part of the official website. For example, you can see the Tesla investor platform: https://ir.tesla.com/#quarterly-disclosure

You can also use online platforms like Yahoo Finance, TIKR, and others. They show all the financial statement data and have handy tools, like ratios. We like using these platforms because they give us a neat way to see the important information at first glance.

After you take a first peak at the company's financial information through screeners like Yahoo Finance, you can go on and readan read a 10-K form of a company. The 10-K form is a critical resource with much more company information. It provides detailed insights into a company's operations, financial condition, and future prospects. This document is particularly crucial for US-based companies, with a variant called 20-F available for foreign companies listed on the US market. A reliable source to access these forms is the EDGAR (Electronic Data Gathering, Analysis, and Retrieval system) database, powered by the US Securities and Exchange Commission, which ensures the authenticity and accuracy of the information provided.

Now, once you actually open such a 10-K, you might say that it is long and boring. Unfortunately, that is the reality, but you have to read them; they are probably the most complete set of information out there you might find. Nevertheless, remember that information is always distorted; your duty is to find a more reliable source and stick with it.

So, after you’ve potentially found a company that you’re interested in and the first information seems promising, you can start to verify whether the story (qualitative) matches the numbers (quantitative). We will do this by looking deeper into the Financial Statements and Ratios of the company. Remember that numbers alone are not enough; they can always be distorted with accounting tricks; try to see the whole picture. This is the part where everything comes together.

“Investing in stocks is an art, not a science, and people who’ve been trained to rigidly quantify everything have a big disadvantage.”

Peter Lynch

Financial Statements

We know that financial statements might look intimidating at first, but it’s actually all simple math maths and you should not be afraid of it. We recommend watching the course by Prof. Aswath Damoradan (Stern University, NY) Accounting 101, who explains everything you need to know to understand the basics. These basics will already help you a lot in conducting your quantitative analysis. Unfortunately, a blog post is not enough to cover everything in detail, so we actually recommend doing a lot of further reading to understand different scenarios, as other industries will have slightly different numbers. Numbers that might be considered bad in one industry could be regarded as good in another industry.

“Examples abound of how considerable increases in inventory and/or accounts receivable can forecast downward earnings and surprises. This is especially true in those industries subject to rapid changes in products and taste. Expect to find them in companies dealing with high fashion, seasonal goods, and especially high tech. No investor seriously involved with stocks in these industries can afford to ignore accounts receivable and inventories.”

Thorton L. O'Glove, Quality of Earnings

We will look at the three most important financial statements and give you a rough overview to get you started:

- Balance Sheet: The Balance Sheet offers a snapshot of a company’s assets, liabilities, and shareholders' equity at a specific point in time, allowing investors to assess the company’s financial stability and liquidity.

- Income Statement: The Income Statement details a company’s revenues, expenses, and profits or losses over a specified period, serving as a tool for investors to gauge profitability, efficiency, and growth prospects.

- Cash Flow Statement: The Cash Flow Statement records the cash generated or expended by a company in a given period across operating, investing, and financing activities, which is pivotal for investors seeking to understand a company’s cash-generating abilities and financial robustness.

Balance Sheet

The key learning from the Balance Sheet is what the company owns and owes, as well as the amount invested by shareholders; understanding this is vital as it showcases the company’s net worth and its ability to meet its obligations and invest in future growth.

- Current Ratio (Current Assets / Current Liabilities): A ratio above 1 indicates that the company can pay off its short-term obligations, with a ratio of 2 or above being considered healthy.

- Debt-to-Equity Ratio (Total Debt / Total Equity): A ratio under 1 is preferable, signalling lower financial risk, while a high ratio indicates higher reliance on debt and potential risk.

- Return on Equity (Net Income / Shareholder’s Equity): A ratio above 15% is considered good, indicating effective use of shareholders’ equity to generate profits.

Income Statement

The key insight gained here is how well a company can generate profits from its operations; a higher net income and consistent profits over time are indicative of a company’s ability to effectively manage its resources and grow.

- Net Profit Margin (Net Income / Revenue): A high ratio, generally above 10%, is favourable, showing a significant portion of revenue is retained as profit.

- Earnings Per Share (EPS) (Net Income / Number of Outstanding Shares): A higher EPS is better, indicating more profit allocated to each share of common stock.

- Price-to-Earnings Ratio (P/E) (Market Value per Share / EPS): A P/E ratio under 15 is often considered a sign of an undervalued stock.

Cash Flow Statement

A positive operating cash flow, along with a healthy free cash flow after capital expenditures, indicates that the company is generating sufficient cash from its core business operations to sustain itself and potentially invest in growth.

“Expected long-term cash flows, discounted by the cost of capital—not reported earnings—determine stock prices.”

Michael J. Mauboussin, Morgan Stanley

- Operating Cash Flow: Positive cash flow is essential, showing the company can generate sufficient cash from operations.

- Free Cash Flow (Operating Cash Flow – Capital Expenditures): Positive free cash flow is desirable, indicating the availability of cash for shareholders after investments.

- Cash Conversion Cycle: A shorter cycle is better, indicating efficient conversion of investments into cash.

Financial Ratios

As Graham is sort of the godfather of value investing and added a lot of value to the world of fundamental analysis, here are some metrics that he would consider useful. It’s also crucial to note that these ratios and metrics should never be used in isolation but should be part of a comprehensive analysis of a company's financial health, growth prospects, competitive position, and the broader market and economic environment. So, for example, in the previous years, interest rates have been historically low, and thus, stock market valuations have generally been higher and analysts might be more flexible with higher P/E ratios, especially for growth stocks or stocks in sectors like technology.

- P/E Ratio Under 15: Signals potential undervaluation of the stock.

- Current Ratio Over 2: Denotes strong short-term financial stability.

- Debt-to-Equity Ratio Under 1: Indicates lower financial risk.

- Earnings Growth Over 5% Annually: Represents promising growth prospects.

- High Dividend Yield: Can signify a value investment when analyzed with other metrics.

- Return on Equity Over 15%: Reflects efficient use of shareholders' equity to generate profits.

Earnings Reports

In conclusion, we will briefly discuss two key financial metrics: Earnings Per Share (EPS) and Price-to-earnings ratio (P/E), which are essential for assessing a company's financial standing.

Earnings Per Share (EPS)

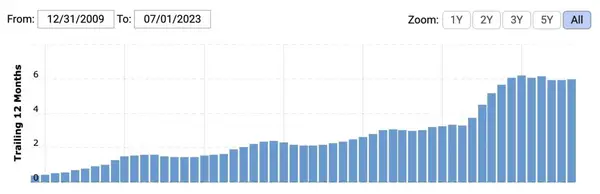

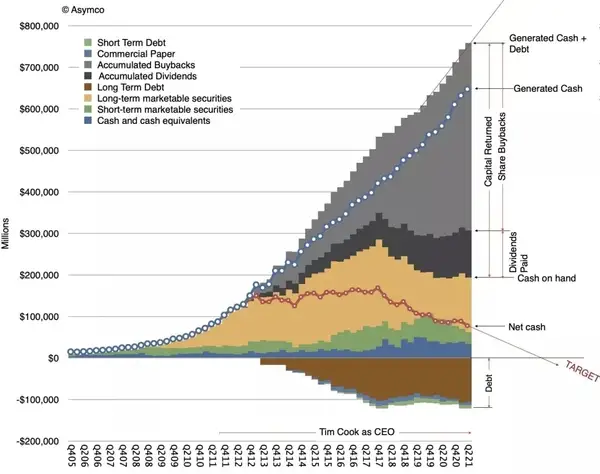

EPS represents a company’s profit divided by the number of outstanding shares. For example, if Apple has a net income of $50 billion and 10 billion shares outstanding, its EPS would be $5. This figure is a quick indicator of profitability, but it's important to consider how share buybacks, a practice used to reduce the number of shares and potentially increase EPS, might affect this value. In the charts below, you can see how the Apple EPS developed. The first chart shows that in 2009, it was below $1 and rose to over $5. In the second chart, you can see, in the grey area, how buybacks actually affected the value significantly.

Investors should seek consistent EPS growth while also examining the company’s overall financial health. For example, take a look at Enron, which filed for bankruptcy in 2001; their EPS was mostly positive, yet their free cash flow was negative.

Price to Earnings Ratio (P/E)

P/E ratio tells us how much investors are willing to pay for each dollar of earnings. It's calculated by dividing the stock price by the EPS. A lower P/E might suggest that the stock is undervalued, but growth prospects are also crucial. For instance, a stock with a P/E of 30 and an earnings yield of 3.3% could be appealing if the anticipated growth rate is high. It’s crucial to make conservative estimations and apply a margin of safety when using this metric to account for

uncertainties.

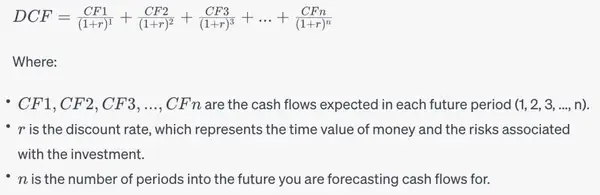

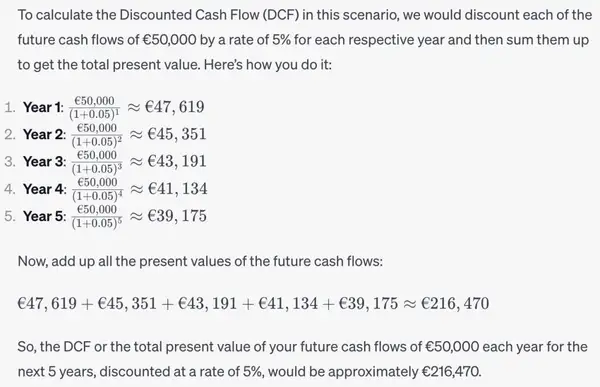

Valuation Methods

Once again, valuation is a big topic and you should do more research on this on your own. In short, we will give you a glimpse of the main valuation method, Discounted Cash Flow. It is used to calculate the value of an investment based on future cash flows.

- You estimate how much money the business will generate in the future

- And you discount the value back to the amount it would be worth today

As some are more practical learners, here is an easy-to-understand example of how to calculate the Discounted Cash Flow (DCF)

This method is probably one of the most straightforward ones. However, there are many other valuation methods that are used, depending on what you want to achieve. As you saw, there are already tons of different metrics to look at, ratios to calculate, and valuation methods to consider. Remember, with every additional variable, you also add additional complexity to your analysis – so try to follow Einsteins' advice:

“Everything should be made as simple as possible, but no simpler.”

Risks Involved in Fundamental Analysis

Risk. It's probably one of the most important things to consider. Risk is what separates gamblers from investors. It is not exactly about how much risk you take but more about your relationship with it. Fundamental analysis is not a mathematical formula; it is not precise. As many professionals say, investing is an art. This also encompasses the extreme complexity of investing; one does not just “solve” the financial markets, except Jim Simons for a time maybe. Remember the statistic from the beginning? Only around 5-10% of professional investors actually beat the market over 15 years. Overconfidence will drown you in the sea of reality like it has so many other people who have lost billions of dollars in the financial markets. Not investing is risky, but investing without being aware of the risks is foolish. Investing is a serious business with many risks involved, so take it seriously.

“Although it’s easy to forget sometimes, a share is not a lottery ticket… it’s part-ownership of a business.”

Peter Lynch

Conclusion

Bravo! You’ve battled through the wilderness of fundamental analysis and emerged with your wits intact. Give yourself a pat on the back – you’ve earned it! So, what’s next on the agenda? Ditch the days of snapping up stocks based on coffee shop gossip and dive headfirst into the real game.

Roll up your sleeves and get those hands dirty! Pick a sector that interests you, start learning about the companies there, and put that fundamental analysis knowledge to the test. Remember, it's time to be the Sherlock of stocks, not the gambler at the roulette table.

“Buying stocks without studying the companies is the same as playing poker — and never looking at your cards.”

Peter Lynch

Disclaimer: All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs. This post does not constitute investment advice.

Painless trading for everyone

Hundreds of markets all in one place - Apple, Bitcoin, Gold, Watches, NFTs, Sneakers and so much more.

Painless trading for everyone

Hundreds of markets all in one place - Apple, Bitcoin, Gold, Watches, NFTs, Sneakers and so much more.